This example provides an opportunity to practice calculating the overhead variances that have been analyzed up to this point. This is a portion of volume variance that arises due to high or low working capacity. It is influenced by idle time, machine breakdown, power failure, strikes or lockouts, or shortages of materials and labor. If the outcome is favorable (a negative outcome occurs in the calculation), this means the company was more efficient than what it had anticipated for variable overhead.

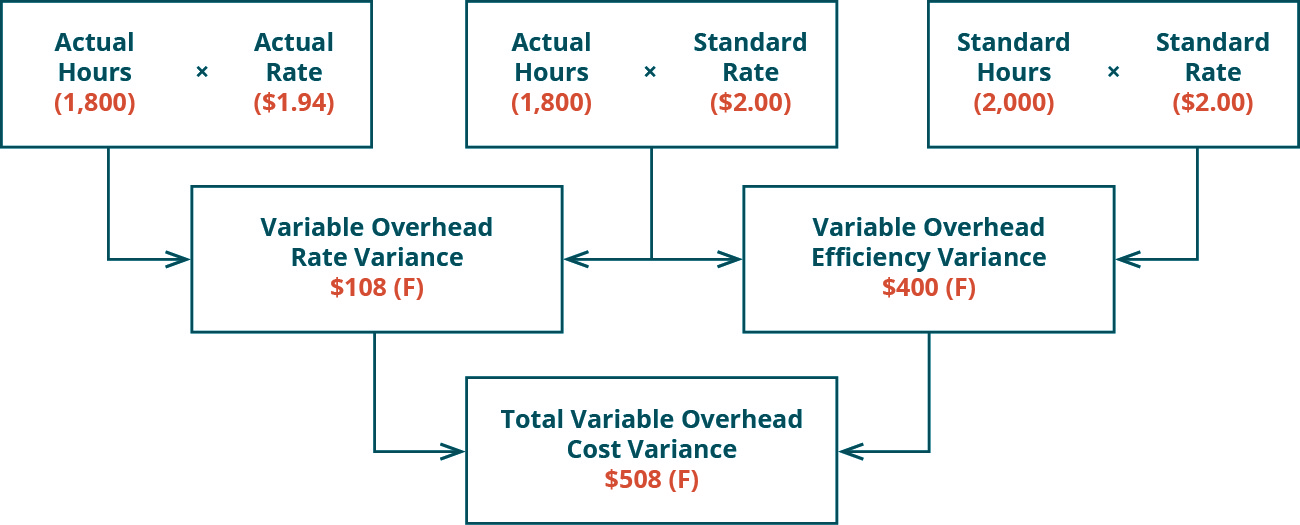

Determination of Variable Overhead Rate Variance

Standard fixed overhead costs are allocated to production based on the standard rate which is calculated using the budgeted production volume. If the actual production volume is not the same as the budgeted production volume then there will be a variance between the budgeted fixed overhead and the standard fixed overhead. The standard overhead rate is the total budgeted overhead of $10,000 divided by the level of activity (direct labor hours) of 2,000 hours.

Determination of Variable Overhead Efficiency Variance

Figure 10.14 summarizes the similarities and differences betweenvariable and fixed overhead variances. Notice that the efficiencyvariance is not applicable to the fixed overhead varianceanalysis. A favorable variance means that the actual variable overhead expenses incurred per labor hour were less than expected. Suppose Connie’s law firm finances: bookkeeping, accounting, and kpis 2023 Candy budgets capacity of production at \(100\%\) and determines expected overhead at this capacity. Connie’s Candy also wants to understand what overhead cost outcomes will be at \(90\%\) capacity and \(110\%\) capacity. It is one of the two parts of fixed overhead total variance; the other is fixed overhead volume variance.

- Connie’s Candy used fewer direct labor hours and less variable overhead to produce 1,000 candy boxes (units).

- However, during the period cost rationalization measures were carried out and fixed overheads were reduced by minimizing inefficiencies resulting in an annual fixed overhead expense of $420,000.

- If DenimWorks pays more than $8,400 for the year, there is an unfavorable budget variance; if the company pays less than $8,400 for the year, there is a favorable budget variance.

- Suppose Connie’s Candy budgets capacity of production at \(100\%\) and determines expected overhead at this capacity.

(ii) Volume Variance

As mentioned above, we will assign the fixed manufacturing overhead on the basis of direct labor hours. A favorable variance means that the actual hours worked were less than the budgeted hours, resulting in the application of the standard overhead rate across fewer hours, resulting in less expense being incurred. However, a favorable variance does not necessarily mean that a company has incurred less actual overhead, it simply means that there was an improvement in the allocation base that was used to apply overhead. Fixed overhead budget variance is favorable when actual fixed overhead incurred are less than the budgeted amount and it is unfavorable when the actual fixed overheads exceed the budgeted amount. Variable overhead spending variance is favorable if the actual costs of indirect materials — for example, paint and consumables such as oil and grease—are lower than the standard or budgeted variable overheads.

The budgeted production volume here is also referred to as the normal capacity of the company or the existing facility in the production. Likewise, if the actual production exceeds the normal capacity, the result is favorable fixed overhead volume variance and vice versa. If the actual production volume is higher than the budgeted production, the fixed overhead volume variance is favorable.

It is the normal capacity that the company or the existing facility can achieve for the period. This figure is usually included in the budget of production that is planned or scheduled before the production starts. In our example, we budgeted the annual fixed manufacturing overhead at $8,400 (monthly rents of $700 x 12 months). If DenimWorks pays more than $8,400 for the year, there is an unfavorable budget variance; if the company pays less than $8,400 for the year, there is a favorable budget variance.

Let’s also assume that the actual fixed manufacturing overhead costs for the year are $8,700. As we calculated earlier, the standard fixed manufacturing overhead rate is $4 per standard direct labor hour. This variance would be posted as a debit to the fixed overhead volume variance account. The company can calculate fixed overhead volume variance with the formula of standard fixed overhead applied to actual production deducting the budgeted fixed overhead. Variable overhead spending variance is the difference between actual variable overhead cost, which is based on the costs of indirect materials involved in manufacturing, and the budgeted costs called the standard variable overhead costs.

Fixed manufacturing overhead costs remain the same in total even though the production volume increased by a modest amount. For example, the property tax on a large manufacturing facility might be $50,000 per year and it arrives as one tax bill in December. The amount of the property tax bill did not depend on the number of units produced or the number of machine hours that the plant operated.

The variance is calculated the same way in case of both marginal and absorption costing systems. Specifically, fixed overhead variance is defined as the difference between standard cost and fixed overhead allowed for the actual output achieved and the actual fixed overhead cost incurred. The fixed factory overhead variance represents the difference between the actual fixed overhead and the applied fixed overhead.

Fixed Overhead Expenditure Variance, also known as fixed overhead spending variance, is the difference between budgeted and actual fixed production overheads during a period. As an example of an unfavorable fixed overhead spending variance, a passing tornado delivers a glancing blow to the production facility of Hodgson Industrial Design, resulting in several hundred roofing tiles being blown off. This cost is part of the facilities maintenance budget, which normally does not vary much from month to month, and so is part of the company’s fixed overhead. The fixed manufacturing overhead volume variance is the difference between the amount of fixed manufacturing overhead budgeted to the amount that was applied to (or absorbed by) the good output. If the amount applied is less than the amount budgeted, there is an unfavorable volume variance.

The journal above now allocates some of this expense (11,000) to production, this is represented by the credit entry to the expense account. If the actual amount spent on fixed overhead is not the same as the amount budgeted for fixed overhead, then there will be a variance known as the fixed overhead budget variance. Controlling overhead costs is more difficult and complex than controlling direct materials and direct labor costs. Variable production overheads include costs that cannot be directly attributed to a specific unit of output. Costs such as direct material and direct labor, on the other hand, vary directly with each unit of output. On the other hand, the budgeted production volume is the production volume that the company estimates to produce or achieve during the period.